What Is Non Agricultural Income

What Is Non Agricultural Income, Indeed recently has been hunted by consumers around us, perhaps one of you personally. People now are accustomed to using the internet in gadgets to view video and image information for inspiration, and according to the name of this article I will discuss about

If the posting of this site is beneficial to our suport by spreading article posts of this site to social media marketing accounts which you have such as for example Facebook, Instagram and others or can also bookmark this blog page.

Http Citeseerx Ist Psu Edu Viewdoc Download Doi 10 1 1 460 6790 Rep Rep1 Type Pdf Attestation De Deplacement Professionnel France Belgique

Agricultural Progress And Poverty Reduction Oecd Attestation De Deplacement Professionnel France Belgique

Big Income Tax Query Answered Nris Are Subject To Tax In India Only In Respect Of India Sourced Income The Financial Express Attestation De Deplacement Professionnel France Belgique

1 Share Of Agricultural And Non Agricultural Income In The Total Income Download Scientific Diagram Attestation De Deplacement Professionnel France Belgique

Agricultural Income Attestation De Deplacement Professionnel France Belgique

Ppt Agricultural Income Powerpoint Presentation Free Download Id 1696768 Attestation De Deplacement Professionnel France Belgique

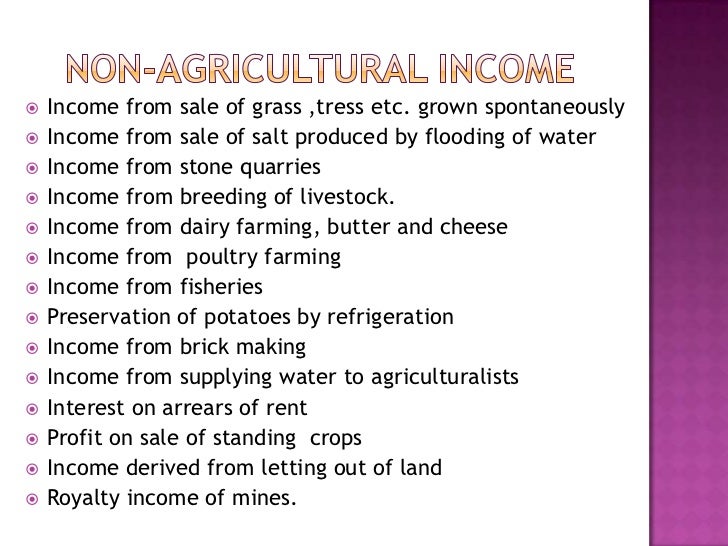

Income from sale of land is capital gain income and not agricultural incomeincome from use of buildinghouse attached to land for any business or profession or letting for use as business or professionincome from performing only subsequent operations is not agricultural incomecommission earned by br.

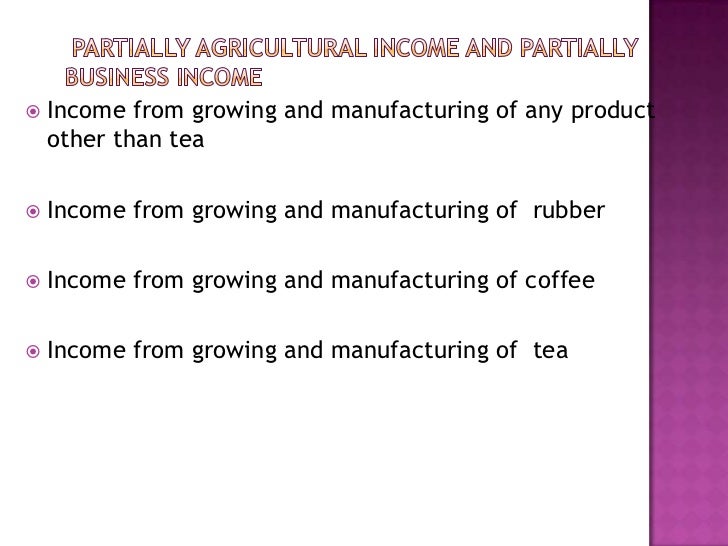

Attestation de deplacement professionnel france belgique. Agricultural income refers to income earned or revenue derived from sources that include farming land buildings on or identified with an agricultural land and commercial produce from a horticultural land. Partial agriculture income is the income where assessee is growing agriculture produce and use them as raw material for manufacturing of products. They are as follows.

Such a situation arises in case of certain agro based industries where agricultural produce is used as raw material and it ie raw material is produced by the same person ie industrialist who manufactures industrial product by using such raw material. Revenue from the sale of processed products of agricultural nature without actual agricultural activity. The product must be produced by employing the human labour.

The primary sector that is agriculture contributed 60 or more of the total income and two thirds of total people employed were in the agriculutral sector. Here income from the sale of product is partial agriculture income and partial non agriculture income. The non agricultural income of the taxpayer exceeds the maximum amount non chargeable to tax.

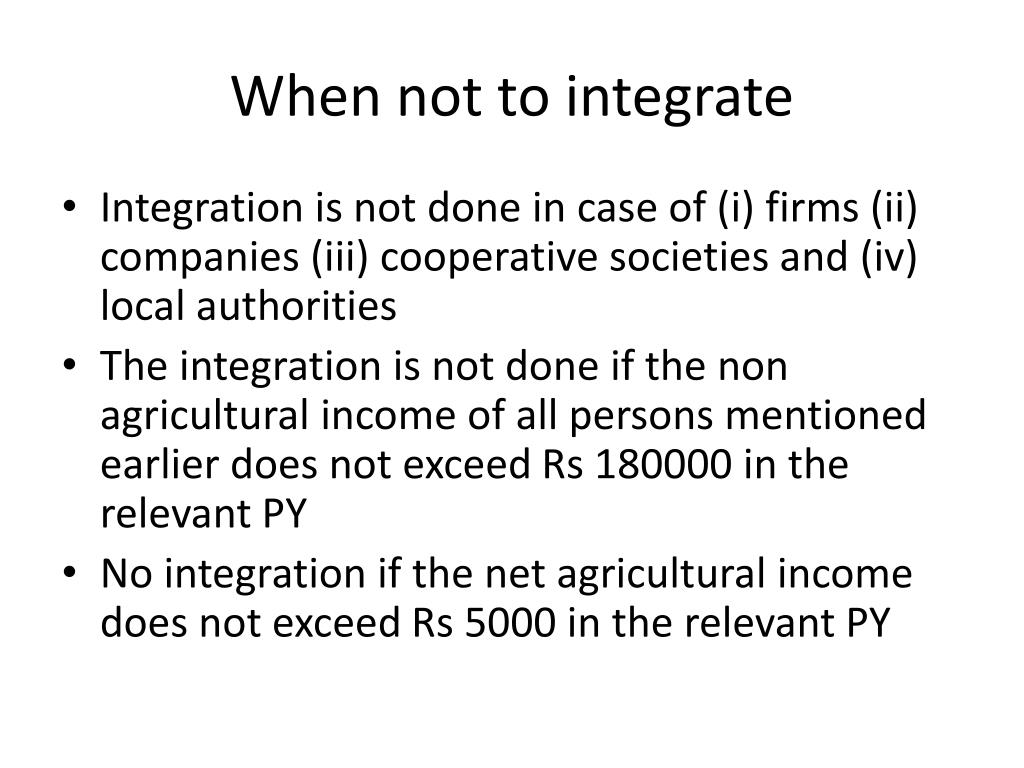

The need to do so would arise only if his net agricultural income is greater than rs 5000 during the year and his non agricultural income is higher than the maximum amount not chargeable to tax under the tax slab. Sometimes income comprises of both agricultural as well as non agricultural income. The below mentioned list draws exception to that revenue or income which is generated by doing agriculture work but they are non agriculture income.

According to this section agricultural income generally means. If a farmer is generating agricultural income along with non agricultural income he will have to calculate the taxable income. Agriculture income is exempt under section 101 of the indian income tax act but while computing tax on non agricultural income agricultural income is also taken into consideration and when we compute tax taking agriculture income into consideration we pay tax on agriculture income also.

If any thing which is produced from the land without human effort then it will be called non agricultural income. Of age and rs300000 for the individual above than 60 yrs of age. Non agricultural income should exceed the amount of rs250000 for the individual below than 60 yrs.

Agricultural income is defined under section 21a of the income tax act 1961.

2 Attestation De Deplacement Professionnel France Belgique

Https Www Jstor Org Stable 4362873 Attestation De Deplacement Professionnel France Belgique

Income Tax Treatment Of Agricultural Income Capital Gains Tax Agriculture Attestation De Deplacement Professionnel France Belgique

Agricultural Income Attestation De Deplacement Professionnel France Belgique